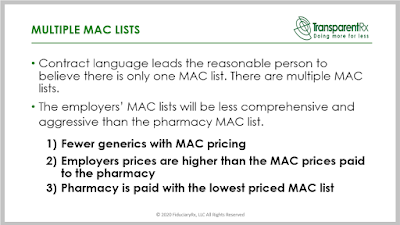

Three surefire ways to know if your PBM is overcharging you

Pick anyone from HR, finance or procurement and they will tell you succinctly the pharmacy cost trend is not sustainable. Most have tried every trick in the book including increasing employee cost share, restricting access or reducing benefit levels. But, ask these same professionals how much money their PBM is making and you’ll likely get crickets. It is not uncommon for the non-fiduciary PBM’s take home to amount to more than the cost of the prescription drugs.

I’ll let the note Michael Critelli, former CEO at Pitney Bowes, sent to me address that point. “I am pleased that you wrote the particular essay I downloaded. Many corporate benefits departments do not understand that they are overmatched in negotiating with pharmacy benefit managers, as are the “independent consultants” who routinely advise them. The first step in being wise and insightful is admitting what we do not know, and you have humbled anyone who touches this field.”

For those interested in improving their company’s pharmacy benefit management results and unafraid of unconventional concepts, here are three surefire ways to know if your PBM is overcharging you.

1) Contract definition for brand and generic drugs. Brand Drug means a prescription product identified as a “brand” by Acme PBM or its designee using indicators from reporting services such as First Databank or other third party reporting sources. If your definition for brand or generic drugs looks remotely close to the example above, then you are being overcharged.

2) Contract definition for rebates. The definition for rebates in your contract should not include any exclusions or limitations. Strike any language that reads similar to Rebates do not include administrative fees paid by Pharmaceutical Manufacturers, Rebates do not include purchase discounts paid by Pharmaceutical Manufacturers, or directly attributable to the utilization.

3) Low or no administrative fee. An artificially too low administrative fee is a dead giveaway for overpayments. This is especially true when the plan sponsor has no audit rights on pharmacy reimbursements, no ability to determine net costs through NDC claim level detail for rebates, or finally little input on benefit design beyond member cost share, for instance.

Managing the pharmacy benefit efficiently is no easy task. It requires quite a bit of time, effort and skill to do it right. Anyone with business training can look at a P&L statement and determine whether or not a company made a profit. However, understanding the story behind those numbers requires a certain set of skills only a certified public accountant can provide, for example. The same can be said for pharmacy benefits as it too requires a particular set of skills and values to achieve lowest net cost.