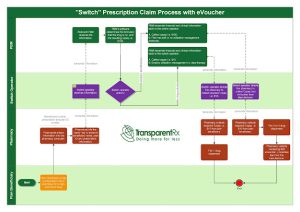

Tip of the Week: eVouchers help circumvent health plan sponsor benefit designs to get high-cost brand drugs dispensed

Brand drugmakers are circumventing pharmacy benefit plan designs by offering eVouchers or electronic vouchers for expensive drugs at the “Switch.” Why aren’t more people outraged about this? The switch is what routes the third-party prescription claims to the PBM or health plan associated with the prescription. Within seconds, the script leaves the pharmacy, goes to the switch, and then is received at the relevant PBM.

- Doctors “set aside concerns over costs”

- “Patients benefit from lower copays” and “increased adherence”

- Manufacturers benefit from increased “scripts written”, “the likelihood patients will fill and adhere to them” and “increased brand loyalty”

|

| Click to Enlarge |

There are two ways to prevent the scenario above from happening:

(1) PBM inserts language into its contract with the Switch company, preventing the action.

(2) Benefit design maximizes the drug utilization management toolkit including step therapy and mandatory generic enforcement programs.

Number two is sticky as many plan sponsors are hellbent on employees getting the drug they want without any scrutiny (i.e. step therapy). I don’t agree but it’s not my checkbook. The point is to make people happy through better outcomes not for the sake of avoiding the pain that comes with running an efficient health plan. In a sense, drugmakers, and non-fiduciary PBMs for that matter, are leveraging HR’s desire to keep employees “happy.”

For TransparentRx the choice is simple, either you want an efficient pharmacy benefit program or you don’t. If you [health plan sponsors] don’t want an efficient pharmacy benefit program then expect to pay $1000 for a drug when a $100 drug would have provided the same level of efficacy, for example. eVouchers, especially when supported with direct-to-consumer TV ads for high-cost brand drugs and soft utilization management protocols, are an expensive proposition for health plan sponsors yet lucrative one for brand drugmakers.